H:thin-market-supplier-leverage — The deep-market null is not universal: a bounded within-firm gap in thin and early cells¶

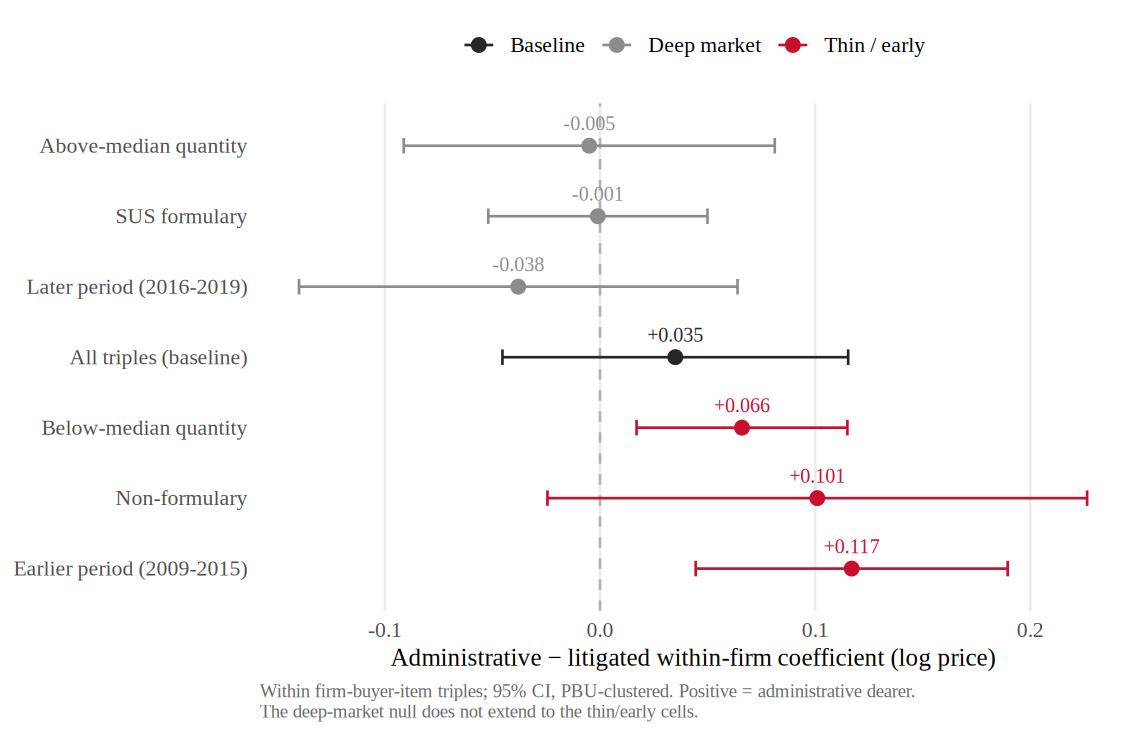

The within firm-buyer-item null tells us there is no broad same-firm markup in deep repeated urgent markets (H:no-broad-same-firm-markup). But that null is a deep-market statement, and the natural follow-up is: where the incumbent supplier has fewer alternatives — small lots, drugs off the public formulary, the earlier years before the urgent market matured — does the markup come back? Partly — but not as supplier leverage. Cutting the within-triple sample by market depth, the administrative-vs-litigated coefficient does turn positive in the thin and early subsamples, but disambiguating the two axes shows the quantity dimension is the scale channel (not same-firm pricing) and the surviving earlier-period gap is administrative-dearer and fades over time — the opposite direction from a court order squeezing the sanctioned buyer. What survives is a bounded statement: the deep-market null is not universal, with a residual within-firm gap in the earlier period.

Economic intuition

The deep-market result said the same supplier does not, on average, charge more under a court order. But "on average, in deep markets" is a scoped claim. When the order is small, when the drug is not on the standard public formulary, or when we look at the earlier years before the urgent market filled in, a same-firm price difference reappears. The follow-up tests show exactly how to read that fact: the quantity axis is scale, and the surviving early-period gap is administrative-dearer, not litigated-dearer. The evidence therefore supports a bounded non-null: the deep-market null is not universal, but this is not a clean claim that court sanctions let suppliers squeeze litigated buyers.

Evidence strength: Partial (strongly supported). The within firm-buyer-item heterogeneity in AN-003 shows the Admin coefficient flat or null in deep markets (above-median quantity −0.005; SUS-formulary −0.001) but positive and significant in thin and early markets (below-median quantity +0.066, ; earlier period +0.117, ; non-formulary +0.101). AN-004 organizes these splits by market depth. Two referee tests disambiguate the result: the quantity axis is the scale channel (within-FBI log-quantity −0.259; the gradient collapses under a quantity control), and the earlier-period gap survives a within-triple quantity control (+0.117 → +0.168, p = 0.007) but is administrative-dearer and time-declining — a genuine residual within-firm gap in the earlier period, not litigated-buyer leverage. The status is therefore Partial (strongly supported) for the bounded non-null: the deep-market null is not universal. The interpretation remains disciplined, because the surviving gap is not the "supplier squeezes the sanctioned buyer" channel.

Theory¶

Supplier market power is a function of the buyer's outside options. When a buyer can credibly source the same molecule from many firms — deep, repeated, formulary-listed markets with large lots — an incumbent has little room to extract a markup, which is why the within-triple coefficient is null there. When the buyer's alternatives are thin — small one-off lots, non-formulary drugs with few qualified suppliers, the early years before the urgent procurement market matured — a same-firm price gap is more likely to appear. This is the standard logic of accountability and supplier power (Prendergast, 2007) interacted with market structure, but the sign matters: one-sided pressure to deliver would predict litigated-buyer vulnerability, while the surviving period gap is administrative-dearer. The result is not a contradiction of the deep-market null; it is the same accountability mechanism with an explicit boundary on what the current evidence can claim.

Prediction¶

The within firm-buyer-item administrative coefficient should be near zero in deep markets (above-median quantity, formulary drugs) and positive and significant in thin and early markets (below-median quantity, non-formulary drugs, earlier period). The contrast across these splits is the test.

Competing prediction¶

Uniform null (leverage absent everywhere). A reading of the deep-market null as universal would predict that the within-triple coefficient stays near zero on every subsample. The heterogeneity rejects this: below-median quantity (+0.066, ) and earlier period (+0.117, ) are positive and significant. A second alternative is that the thin-market positives are pure small-sample noise; the consistency of the sign across three theoretically motivated splits (quantity, formulary status, period) and the significance stars weigh against pure noise, though the cells are smaller than the pooled deep-market sample, so the status is partial-strong for the bounded non-null rather than for a universal supplier-leverage interpretation.

Setting evidence¶

Urgent pharmaceutical procurement in São Paulo spans a wide range of market depths within the same regime contrast: large recurring orders of common formulary drugs sit alongside small one-off purchases of niche, non-formulary molecules, and the urgent procurement market itself thickened over the 2009–2019 window. This within-setting variation in supplier alternatives is what lets the same within-triple design speak to both the deep-market null and the thin-market leverage result. See docs/paper.md for how formulary status and lot size enter the data.

Empirical test¶

- Outcome variable: log negotiated price.

- Variation: administrative vs litigated within firm-buyer-item triples, interacted with market-depth proxies.

- Splits: above- vs below-median quantity; SUS-formulary vs non-formulary; earlier vs later period.

- Specification: within-triple fixed-effects regression estimated separately on each subsample (same design as AN-003).

- Sample: the 4,573-observation, 1,206-triple within-triple panel, partitioned by depth.

Data requirements and limitations¶

Requires the same within-triple urgent panel as H:no-broad-same-firm-markup, partitioned by market depth. The thin-market cells are smaller than the pooled sample, so the leverage estimates are noisier and the result is best read as a consistent pattern across theoretically motivated splits rather than a precise magnitude for any single cell. The splits are descriptive partitions, not a randomized manipulation of market depth, so they show where leverage concentrates, not a causal effect of thinning a market.

Evidence¶

| Analysis | Bearing | Key takeaway |

|---|---|---|

| AN-003 | Supports | Heterogeneity in the within-triple coefficient: deep markets flat (above-median quantity −0.005; SUS-formulary −0.001); thin/early markets positive and significant (below-median quantity +0.066 ; earlier period +0.117 ; non-formulary +0.101). |

| AN-004 | Supports | Organizes the within-triple splits by market depth; the deep-market null is not universal, but the sign and scale diagnostics bound the supplier-leverage interpretation. |

Read alongside the deep-market null in H:no-broad-same-firm-markup: the two together make the scope claim that the same-firm margin is deep-market null, thin-market positive.

Open tests¶

Multiple-testing and continuous interaction (run)¶

We probe the two obvious threats — that the splits are multiple-testing

artifacts, and that the quantity axis is an arbitrary dichotomy

(analysis/60_referee_tests.R). The subsample markups survive multiple-testing

correction: under Holm the below-median-quantity coefficient has adjusted

\(p = 0.041\) and the earlier-period coefficient \(p = 0.010\); a Romano-Wolf free

step-down (PBU cluster bootstrap) gives \(p = 0.053\) and \(p = 0.025\). So the

reappearance is not a data-mined artifact.

The quantity axis, however, turns out to be the scale channel, not same-firm

leverage (analysis/61_h4_quantity_quartiles.R). A quartile decomposition of

the within firm-buyer-item coefficient is monotone in order size — \(+0.285\) at

the smallest orders, then \(+0.063\), \(-0.042\), and \(-0.174\) at the largest — but

that gradient collapses once log-quantity is held fixed within the triple

(\(+0.103\) at Q1, \(+0.181\) at Q4, neither robust), while the within-FBI

log-quantity coefficient is \(-0.259\) (SE \(0.074\)): a clean bulk-discount effect.

The raw quantity gradient is therefore the scale/sourcing channel leaking

through (consistent with H:lost-scale), not a same-firm

pricing gradient.

The earlier-period contrast, by contrast, is not scale

(analysis/62_h4_period_axis.R). Re-estimating the within firm-buyer-item

administrative coefficient on the early and late subsamples with a within-triple

log-quantity control, the early-period coefficient is \(+0.117\) (SE \(0.037\)) and

rises to \(+0.168\) (SE \(0.062\), \(p = 0.007\)) once quantity is held fixed — it

survives, and even strengthens, the scale control, whereas the late-period

coefficient is null throughout (\(-0.038 \to -0.004\) with control). The early

period does have smaller orders (mean log-quantity \(6.20\) vs \(7.98\) late), but

the price difference is not coming from that: it is a genuine within-firm price

gap. A continuous administrative\(\times\)year interaction confirms the same

direction — the within-firm administrative premium declines over calendar

time (\(-0.025\) per year, \(-0.019\) with the quantity control), consistent with

a margin that fades as the urgent market thickens.

Sign caveat — read honestly. The surviving early-period coefficient is positive, i.e. the administrative channel is dearer within firm-buyer-item, not the litigated one. That is a genuine, scale-robust, time-declining same-firm price difference, but it is not the "court order lets the supplier squeeze the sanctioned (litigated) buyer" direction — if anything it points the other way. So the period result firmly establishes that the deep-market null is not universal (a real within-firm gap persists in the early, thin years), but whether to label that gap "supplier leverage" is exactly what the open test below must settle. The status is Partial (strongly supported) for the bounded claim: the quantity axis is reclassified as scale, the period axis is a genuine non-null, and the direction of the period gap is flagged as an open interpretive question rather than asserted as litigated-buyer leverage.

Distinguish thinness from earliness — and pin the sign¶

The disambiguation above leaves one sharp question. Below-median quantity, non-formulary status, and earlier period all proxy for thin supplier alternatives but are correlated, and we now know the quantity axis is scale while the period axis is a genuine within-firm gap. What we do not yet know is why the period gap is administrative-dearer rather than litigated-dearer. A joint specification that separates the market-thinness channel from a pure time-trend / vintage channel — and that models the direction of the gap (does the early administrative channel pay more because of immature batching, a different early supplier mix, or genuine early-market supplier power?) — would settle whether "supplier leverage" is the right label or whether the early premium is a maturation artifact. Until then the period gap is reported as a genuine, scale-robust non-null with its direction flagged, not as litigated-buyer leverage.