AN-003: Within-firm-buyer-item pricing under litigation¶

Economic intuition

Hold everything about the transaction fixed except the regime: the same supplier, the same buyer, the same item. Does that one supplier charge more when the purchase is court-mandated? In deep, repeatedly traded urgent markets, the answer is essentially no — the same firm does not post a broad markup. The picture is not uniform, but the exceptions split in two: the small-lot positive reflects scale (bulk discounts), not the same supplier marking up, while a genuine residual within-firm gap survives in the earlier years — and even that gap is administrative-dearer, not the litigated buyer being squeezed. So the cost of litigation is not a blanket same-firm markup.

Question¶

Within the same firm, the same buyer, and the same item, does the same supplier charge a higher price under the litigated urgent regime than under the administrative urgent comparison? Fixing the supplier identity strips out supplier-set reallocation and isolates the same-firm pricing margin.

Design¶

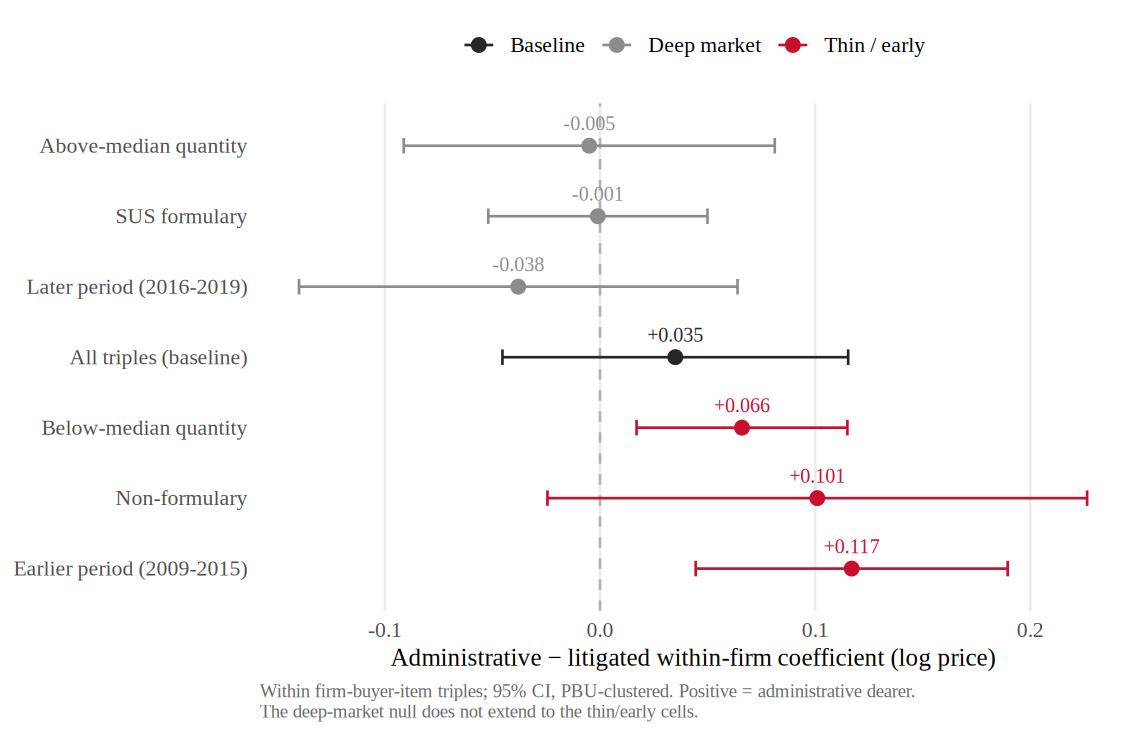

- Sample: firm-buyer-item triples — 4,573 observations across 1,206 triples observed under both urgent regimes.

- Variation: litigated-urgent versus administrative-urgent within the same firm-buyer-item triple.

- Specification: regression of log price on the litigated (versus administrative) urgent indicator, with firm-buyer-item (FBI) and year fixed effects. Standard errors are clustered by PBU.

- Heterogeneity: splits by order quantity (above/below median), formulary status (SUS formulary versus non-formulary), and period (earlier versus later).

Results¶

| Cut | Coefficient (SE) | Reading |

|---|---|---|

| Baseline (all triples) | 0.035 (0.041) | Indistinguishable from zero |

| Above-median quantity | −0.005 | Near zero |

| Below-median quantity | +0.066 (***) | Higher in thin lots |

| SUS-formulary | −0.001 | Near zero |

| Non-formulary | +0.101 | Higher off formulary |

| Earlier period | +0.117 (***) | Higher in early years |

| Later period | −0.038 | Near zero |

FBI + year fixed effects. SE clustered by PBU. *** p<0.01.

Output: v10-causal-mechanism/output/tables/tab_within_firm_robustness.tex.

Interpretation¶

The baseline within-firm coefficient is 0.035 with a standard error of 0.041 — indistinguishable from zero. There is no broad same-firm markup in deep repeated urgent markets: the same supplier, selling the same item to the same buyer, does not post a uniform price premium under litigation. This does not mean the cost margin disappears; it relocates the margin away from same-firm pricing and toward the supplier-set and scale channels documented in AN-005 and AN-006.

The heterogeneity makes the boundary precise, but the thin-market axes behave differently. The below-median-quantity positive (+0.066, ) is the *scale channel, not same-firm pricing: holding firm, buyer, and item fixed, the within-triple log-quantity coefficient is −0.259 (SE 0.074), and the order-size gradient collapses under a quantity control. The earlier-period gap (+0.117, ) survives that control but is *administrative-dearer and time-declining — a genuine residual within-firm gap, not the litigated buyer being squeezed. Off-formulary (+0.101) is positive but not significant. Where the market is deep — large lots, formulary molecules, the later period — the within-firm gap is near zero. The deep-market null is therefore not universal, but the surviving margin is disambiguated rather than read as broad supplier leverage; this is taken up directly in AN-004.

Confidence: yellow. The within-firm-buyer-item design holds supplier identity fixed, the tightest available control on composition, but it conditions on triples that transact under both regimes — itself a selected set — and the administrative urgent channel remains the selected, larger, closest feasible urgent-procurement comparison rather than a random or clean counterfactual. The reading is yellow because the evidence is single-jurisdiction (São Paulo BEC) and from own-project runs.

Follow-ups¶

- Map the thin-market and earlier-market leverage explicitly against market depth and formulary status — see AN-004.

- Reconcile the near-zero same-firm pricing margin with the observed price gap through the scale and supplier-composition channels — see AN-005.

- Confirm that the supplier set, not the supplier's price, moves under litigation — see AN-006.