H:no-broad-same-firm-markup — In deep repeated urgent markets, the sanction-related cost margin does not appear as a broad same-firm markup¶

The under-the-gun gap could arise in two observationally confounded ways: the same supplier could charge a sanctioned buyer more for the same item (a same-firm markup), or the state could end up buying from a different supplier set on different terms (sourcing). To separate them, the paper holds the supplier–buyer match fixed: it looks within firm-buyer-item triples observed under both urgent regimes — same firm, same item, same buyer. In these deep, repeated urgent markets, the administrative-vs-litigated price difference is statistically indistinguishable from zero. The sanction-related cost margin in these markets is therefore not a broad same-firm markup. This is a deep-market null, not a universal one — a residual within-firm gap reappears elsewhere, which is the subject of H:thin-market-supplier-leverage.

Economic intuition

If a court order let suppliers squeeze the state, you would expect the very same firm to charge the very same buyer more for the very same medicine when a sanction is in play. We can check that directly, because some firm–buyer–item combinations show up under both urgent regimes. When we line those up, the price difference is essentially zero. So in the deep, repeated urgent markets where the same supplier keeps selling the same drug to the same buyer, the extra cost is not coming from that supplier marking up the price. It has to be coming from somewhere else — and the rest of the paper points to how the state is forced to buy: smaller lots and a reshuffled supplier set. This is a statement about deep markets, not a blanket claim.

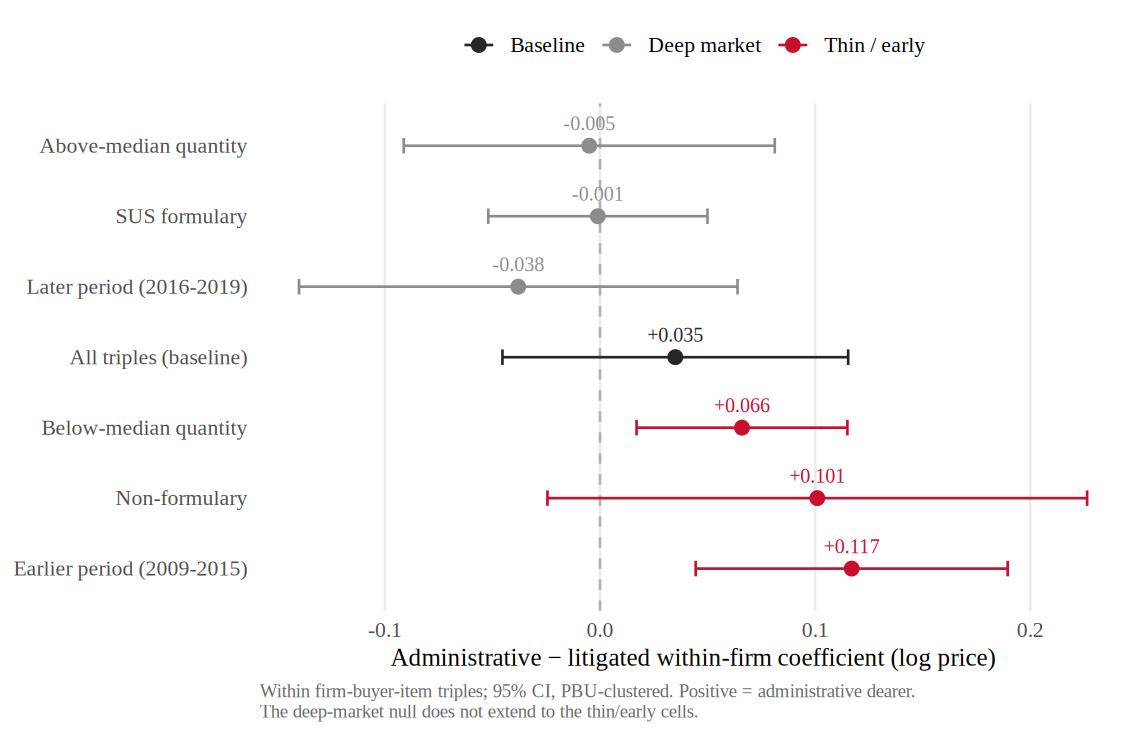

Evidence strength: Partial (strongly supported). Within firm-buyer-item triples (same firm, buyer, item, observed under both urgent regimes), AN-003 reports an Admin coefficient of 0.035 (SE 0.041), statistically indistinguishable from zero — no broad same-firm markup in deep repeated urgent markets. The sample is 4,573 observations across 1,206 triples. The null is a deep-market result, not a universal one: the same analysis surfaces meaningful leverage on thinner and earlier subsamples (see H:thin-market-supplier-leverage).

Theory¶

Accountability models of bureaucratic motivation (Prendergast, 2007) suggest that an agent under one-sided pressure to deliver may accept worse price terms from an incumbent supplier — the supplier, recognizing that the buyer must obtain the good, extracts a markup. This is the same-firm-markup channel: the price difference would show up holding the supplier–buyer–item match fixed. The competing mechanism is the passive-waste / fragmented-sourcing channel (Bandiera, Prat & Valletti, 2009), in which the cost margin instead operates through lost scale and a reallocated supplier set rather than through the incumbent's pricing. The two channels are observationally confounded in any comparison that lets the supplier set vary; the within firm-buyer-item triple is the design that conditions away supplier-set reallocation and isolates same-firm pricing.

Prediction¶

In the within firm-buyer-item triple specification — same firm, same buyer, same item, both urgent regimes — the administrative-minus-litigated price coefficient should be near zero and statistically insignificant in deep repeated markets. If the cost margin were primarily a same-firm markup, this coefficient would be sizable and significant; the prediction here is that it is not.

Competing prediction¶

Incumbent supplier markup (Prendergast-style accountability). The alternative is that the under-the-gun gap is largely a same-firm markup: the incumbent supplier, facing a buyer who must comply with a court order, charges more for the identical item. Under this view the within-triple coefficient should be positive and significant. The deep-market within-triple null (0.035, SE 0.041) rules this channel out as the broad explanation in deep repeated markets. It does not rule it out everywhere: the heterogeneity in H:thin-market-supplier-leverage shows a residual within-firm gap in thinner and earlier cells — though that gap is disambiguated (the quantity axis is scale; the earlier-period gap is administrative-dearer) rather than asserted as litigated-buyer leverage.

Setting evidence¶

The repeated, deadline-driven nature of urgent pharmaceutical procurement generates firm-buyer-item combinations that recur under both the litigated and administrative regimes. Because the same supplier sells the same molecule to the same buyer across regimes, these triples are the natural laboratory for same-firm pricing. The institutional account in docs/paper.md explains how the two urgent regimes share auction procedures, which is what makes the within-triple comparison meaningful.

Empirical test¶

- Outcome variable: log negotiated price.

- Variation: administrative vs litigated regime within a firm-buyer-item triple observed under both.

- Specification: regression of log negotiated price on an administrative indicator with firm-buyer-item fixed effects, so identification comes only from within-triple variation across regimes.

- Sample: 4,573 observations across 1,206 firm-buyer-item triples.

- Heterogeneity splits: above- vs below-median quantity, SUS-formulary vs non-formulary, earlier vs later period (reported under H:thin-market-supplier-leverage).

Data requirements and limitations¶

Requires the BEC urgent panel restricted to firm-buyer-item triples present under both regimes. The within-triple design isolates same-firm pricing at the cost of generalizability: triples that appear under both regimes are, by construction, the deeper and more repeated markets. The null therefore speaks to those deep markets and is explicitly not a universal no-broad-markup claim; thinner and earlier markets, where fewer triples recur, can and do show leverage. The coefficient is a within-triple price difference, not a structural markup parameter.

Evidence¶

| Analysis | Bearing | Key takeaway |

|---|---|---|

| AN-003 | Supports | Within firm-buyer-item triple Admin coef 0.035 (SE 0.041), indistinguishable from zero: no broad same-firm markup in deep repeated urgent markets. 4,573 obs in 1,206 triples. |

See the cross-cutting finding no broad same-firm markup for the claim at full altitude, and H:thin-market-supplier-leverage for where the margin reappears.

Open tests¶

Firm-side heterogeneity in the within-triple null¶

The deep-market null pools across suppliers. Splitting the within-triple coefficient by supplier characteristics (size, market share within the molecule) would show whether the null is uniform across firms or masks offsetting markups and discounts among different supplier types. This sharpens the boundary between the deep-market null and the thin-market leverage result without altering the headline.

Bridge the within-triple null to the decomposition residual¶

The within-firm pricing component enters the Figure 1 decomposition at +3.5% (near zero), consistent with this null. A tighter reconciliation between the within-triple coefficient and the decomposition's within-firm term would consolidate the link from this hypothesis to H:lost-scale.

How this null is bounded — and why it is not "confirmed"¶

This hypothesis is a null, and a null is not the same as proof of zero. The within firm-buyer-item coefficient is 0.035 with a standard error of 0.041, so the 95% interval runs roughly from −0.045 to +0.115: the data show no detectable broad same-firm markup in deep repeated urgent markets, but the interval still admits small same-firm price differences. Absence of a detectable broad markup is not evidence that the markup is exactly zero. The status is therefore Partial (strongly supported) for the bounded, deep-market reading — not "confirmed."

Two further reasons the status cannot be "confirmed":

- The result is not universal by design. A residual within-firm gap persists in thinner and earlier subsamples (H:thin-market-supplier-leverage, below- median quantity +0.066, earlier period +0.117) — though the quantity axis is scale and the earlier-period gap is administrative-dearer, not litigated-buyer leverage. The claim is scoped to deep repeated urgent markets and must stay scoped.

- It is a single-jurisdiction estimate (São Paulo BEC), with no independent cross-data replication.

To bound the null formally, we run an equivalence test on the within

firm-buyer-item coefficient (analysis/60_referee_tests.R). The one-sided upper

95% bound on the coefficient is +0.102, so the deep-market data rule out broad

same-firm markups above about 10.8%. The minimum detectable effect at 80% power

is 12.2%, and power to detect a 10% markup is 0.64; a two-one-sided-tests (TOST)

procedure gives p = 0.070 at a ±10% margin (borderline) and p = 0.364 at ±5%. The

null is therefore genuine against broad markups (anything above ~11% is

rejected) but underpowered against modest ones — which is exactly why the

reading is "no broad same-firm markup," reported as a bound, and not

"confirmed." Cross-jurisdiction replication would be needed to consolidate it

further.

A quartile decomposition confirms the null is not hiding a same-firm pricing

gradient (analysis/61_h4_quantity_quartiles.R): the within-triple coefficient

varies with order size only through bulk discounts — the within firm-buyer-item

log-quantity coefficient is \(-0.259\) (SE \(0.074\)) — and once quantity is held

fixed there is no systematic same-firm price gradient across quantity quartiles.

The order-size variation is the scale channel (H:lost-scale),

not same-firm pricing.