Superseded numbers — canonical-target re-estimation (June 4, 2026)

This analysis note documents a historical run under the earlier validation label. On June 4, 2026 the paper adopted a reproducible, non-circular target (651 always-loser cobidders; frequent-loser flag never used in the label) and re-estimated every result. Where this page conflicts with the paper or the changelog, the paper wins.

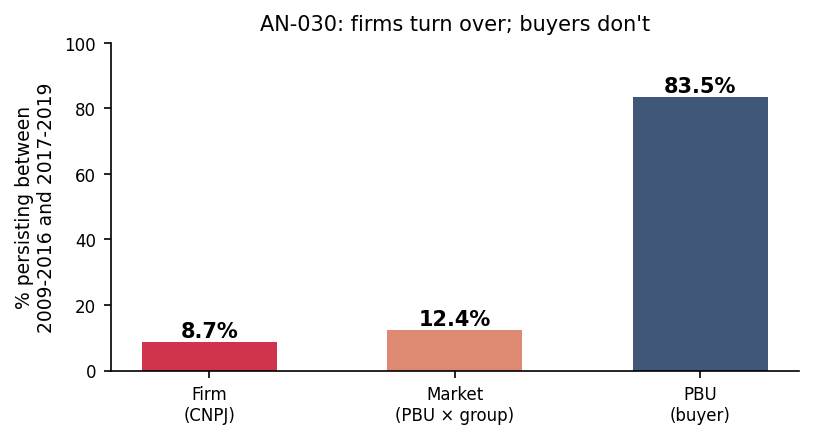

AN-030: Market persistence between early (2009–2016) and late (2017–2019) panel¶

Intuition (plain-language)

Is the temporal holdout a real out-of-sample test or a same-firms reshuffle? Mostly fresh: only 8.7% of firms and 12.4% of markets carry over from the early to the late panel, while 83.5% of buyers persist. So the institutions are stable but the firms and markets being scored are largely new. That asymmetry is what makes the prospective AUC credible — the screen generalizes to new players inside a stable institutional environment rather than re-recognizing old ones.

Question¶

How much do the firms, markets, and procuring buyers in 2017–2019 overlap with those in 2009–2016? The temporal-holdout audits (AN-006, AN-013, AN-029) gain or lose force depending on whether test-period entities are the same firms seen in training. This page documents the structural baseline.

Design¶

- Sample: BEC 2009–2019 panel.

- Early window: 2009–2016.

- Late window: 2017–2019.

- Persistence rate:

(N entities in both windows) / (N entities in early window). - Three units of analysis:

- Firm: identified by CNPJ.

- Market: identified by (PBU × item_group) with ≥5 tenders in the relevant window.

- PBU: procuring buyer (administrative unit).

Results¶

| Unit of analysis | Early N | Late N | Overlap | Persistence (%) |

|---|---|---|---|---|

| Firm | 1,240 | 2,036 | 108 | 8.7% |

| Market (PBU × item-group, ≥5 tenders) | 24,770 | 35,864 | 3,082 | 12.4% |

| PBU | 946 | 1,044 | 790 | 83.5% |

Source: output/market_persistence/persistence_summary.csv.

Figure: persistence rates between 2009-2016 and 2017-2019 panel windows. Firms persist at 8.7% (red); markets at 12.4% (orange); PBUs at 83.5% (navy). The institutional environment is stable; the firm and market populations are essentially fresh across windows.

Interpretation¶

Three readings, all reinforcing H4 (timing discipline):

-

Firm population is essentially fresh between windows. Only 8.7% of early-period firms appear in the late period. The temporal- holdout audits in AN-006 and AN-029 are evaluating a substantially new firm population, not the same firms in slightly different roles. The score generalizes across firms it never saw in training — this is the strongest possible form of within-data out-of-sample evaluation.

-

Market turnover is similarly high. Only 12.4% of early-period (PBU × item-group) markets persist into the late period. The procurement landscape is volatile at the market level — new product-buyer combinations enter, old ones fall off — so the temporal generalization in AN-029 is also testing whether the score's loser-side logic carries across market churn.

-

PBU persistence is high (83.5%) — the procuring buyers are stable. This is consistent with administrative units changing slowly relative to firms and markets. The implication for H4: the institutional environment is stable across the temporal split; the change is in the firms and markets that operate within it. This rules out an alternative reading where the test-period evaluation suffers because procurement institutions changed.

The three-unit pattern is the right baseline for interpreting the temporal-holdout AUC numbers. The temporal AUC of 0.864 (AN-014) and the strict ex ante AUC of 0.767 (AN-006) are NOT explained by "test firms = train firms in disguise" — only 8.7% of firms appear in both windows.

For H:timing-discipline: the structural turnover of firms (~91% replacement) means the temporal holdout is a near-clean out-of-sample evaluation. Combined with the AN-029 result that the cobid_post2019 target (cobidders defined by adjudications AFTER the training window) preserves AUC 0.79–0.89, the timing discipline is about as well-supported as within-data evidence allows.

Follow-ups¶

- Decompose persistence by FL14 status: are FL firms more or less persistent than non-FL always-losers? (relevant for whether FL is a stable firm characteristic vs a state).

- Persistence of cobidders specifically: of the 193 cobidders, how many are in both early and late windows?

- Cross-modality persistence rates.

- Add macros

\valFirmPersist,\valMarketPersist,\valPBUPersistto thescripts/99_make_paper_values.Rpipeline.