Superseded numbers — canonical-target re-estimation (June 4, 2026)

This analysis note documents a historical run under the earlier validation label. On June 4, 2026 the paper adopted a reproducible, non-circular target (651 always-loser cobidders; frequent-loser flag never used in the label) and re-estimated every result. Where this page conflicts with the paper or the changelog, the paper wins.

AN-028: Exposure-stratum balance — cobidders vs reference classes¶

Intuition (plain-language)

Are cobidders just the highest-volume frequent losers wearing a different label? Across seven dimensions — tenders, unique winners crossed, repeat-buyer share, pair density, CADE-facing share, portfolio HHI, number of item groups — they separate from other FLs at effect sizes Cohen's d 0.19–1.00. The distinctness is multi-dimensional, which matters: if it were one-dimensional (just volume) the screen would carry no information beyond a bid counter. AN-041 then asks which dimensions survive once volume is matched away.

Question¶

Within the always-loser stratum, are cobidders distinguishable from non-cobidder FLs along dimensions other than raw participation volume? The exposure question for H3 is: if we hold the stratum fixed and ask whether cobidders look like other FLs, do we see them collapse into a homogeneous "high-volume losers" pool? The standardized-diff battery says no — they remain distinct across multiple dimensions.

Design¶

- Sample: always-loser firms in BEC 2009–2019, partitioned:

- Cobidders: 191 firms (a subset of FL).

- FL_non_cobidder: 2,544 firms (other FL14 firms).

- AL_non_FL: 14,108 firms (always-loser, but below FL14 cutoff).

- winner_other: 24,561 firms (with at least one win).

- Dimensions (7):

tenders_count: participation intensity.unique_winners: count of distinct winners crossed.share_repeat_5: share of buyers with ≥5 repeat interactions.pairs_at_least_5: number of cobidder pairs with ≥5 shared tenders.share_facing_direct_cade: share of tenders where a direct CADE defendant participated.item_group_HHI: portfolio concentration HHI.n_item_groups: number of distinct item groups.- Statistic: Cohen's d (standardized mean difference) and Wilcoxon rank-sum p-value.

Results¶

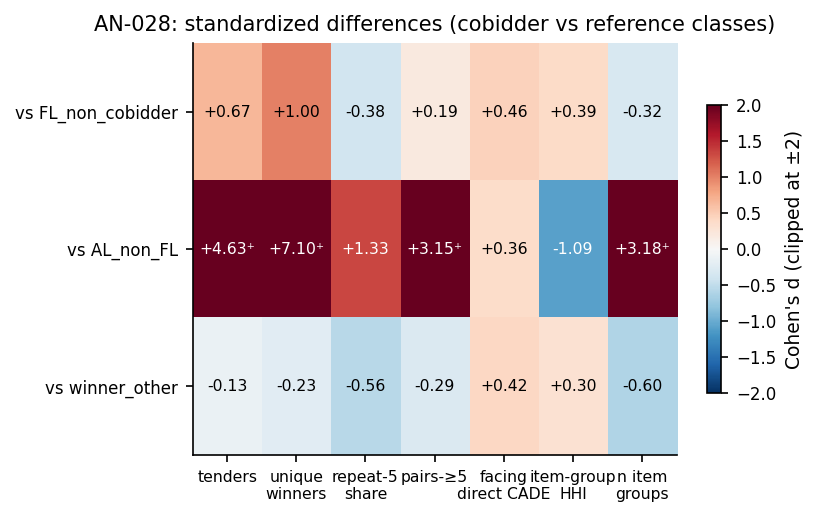

Cohen's d of cobidders vs each reference class, across 7 dimensions:

| Dimension | vs FL_non_cobidder | vs AL_non_FL | vs winner_other |

|---|---|---|---|

| tenders_count | +0.67 | +4.63 | −0.13 |

| unique_winners | +1.00 | +7.10 | −0.23 |

| share_repeat_5 | −0.38 | +1.33 | −0.56 |

| pairs_at_least_5 | +0.19 | +3.15 | −0.29 |

| share_facing_direct_cade | +0.46 | +0.36 | +0.42 |

| item_group_HHI | +0.39 | −1.09 | +0.30 |

| n_item_groups | −0.32 | +3.18 | −0.60 |

All Wilcoxon p-values < 0.05; most < 10⁻¹⁰ — the differences are highly significant given the cobidder N = 191.

Key reading on the vs FL_non_cobidder column (the within-FL14 test that matters for H3):

- Cobidders bid in ~2× more tenders (d = 0.67) and cross ~2× more unique winners (d = 1.00) than non-cobidder FLs. Within the FL stratum, cobidders still have higher participation intensity.

- Cobidders are 8× more likely to face a direct CADE defendant in a tender (1.46% vs 0.17%; d = 0.46).

- Cobidders operate in more concentrated product portfolios (HHI 0.380 vs 0.288; d = 0.39).

- Cobidders are in fewer item groups (7.6 vs 9.5; d = −0.32) — consistent with focal-portfolio cover bidding.

Source: output/theory_bridge/standardized_diffs.csv.

Figure: Cohen's d heatmap of cobidders vs three reference classes (rows) × 7 dimensions (columns). Red = cobidder higher; blue = lower. Values capped at ±2 for color scale; the ⁺ marks cells where the true d exceeds the cap (vs AL_non_FL: d up to 7.1 for unique winners). Cobidder vs FL_non_cobidder is the within-FL row that matters for H3 / H5: d in 0.19–1.00 range across most dimensions.

Interpretation¶

The balance battery answers a key exposure-discipline question: "are cobidders just the highest-participation always-losers?"

The answer is no. Within the FL14 stratum (i.e., conditional on already being a frequent loser):

- Cobidders have higher tenders_count and unique_winners (d 0.67 and 1.00) — the participation margin still discriminates within FL.

- Cobidders have more focal portfolios (HHI d 0.39, n_item_groups d −0.32) — qualitative difference in operations.

- Cobidders are 8× more likely to face direct CADE defendants in a tender (d 0.46) — a structural feature of adjudication-anchored exposure, not a volume artifact.

- Cobidders have lower repeat-buyer shares (d −0.38) — they do not display the "stable supplier" profile of non-cobidder FLs.

For H:exposure-discipline, this means: the FL14 cutoff alone is NOT what concentrates the signal. Even after fixing the always-loser stratum, cobidders remain distinguishable along seven economically meaningful dimensions. The signal carries past volume conditioning.

For H:cobidder-profile-distinct, this is the formal balance table that supports the §5 economic profile of the adjudication-anchored exposure stratum (cobidders are firms with adjudication-anchored exposure to direct CADE defendants, not confirmed cartel members). AN-008 and AN-009 quote selected numbers from this table; this AN documents the full battery.

Follow-ups¶

- Stratify the balance table by procurement modality (Convite vs Pregão).

- Re-run on the audit-disciplined sample (AN-014 OOF folds).

- Match cobidders to non-cobidder FLs on

tenders_countand re-run the balance test — does the remaining signal collapse if we explicitly match on volume? (this is the strongest within-data audit possible for H3). - Add macros

\valDiffTendersFL(0.67),\valDiffUniqueFL(1.00),\valDiffCadeFaceFL(0.46),\valDiffHHIFL(0.39) to the macro pipeline.