Open auctions cut procurement prices by ~10–11% in switched group 65¶

Intuition (plain-language)

In a competitive tender the price is set by whoever goes lowest, and many of the keenest price-cutters are non-SMEs. When São Paulo briefly let them bid for medical supplies and then shut the door again in March 2018, prices tracked the door: about 10–11% lower while open, higher once SME-only returned. The estimate is stable across 6/12/18-month windows. The v8 paper uses this only to pin down timing and sign — the policy magnitude comes from the structural decomposition.

Reduced-form motivation layer

The headline number on this page comes from the v1–v4 reduced-form DiDiR pipeline. The v8 manuscript carries this as motivation in §1 but does not headline it; the v8 canonical claim is the structural decomposition — see Exclusion dominates the price decomposition and Static welfare cost ~28.9%.

🟡 In São Paulo's BEC procurement platform, opening switched group 65 (medical/hospital supplies) to non-SME bidders before March 2018 lowered negotiated prices by ~10–11% relative to the SME-only regime that followed (v8 reduced-form benchmark β = −0.113, 18-month window, item-clustered SEs, p<0.01), identified by a difference-in-differences-in-reverse (DiDiR) against control groups that were SME-only throughout (AN-001). The earlier v1–v4 pipeline gave a slightly larger −0.131 to −0.133; the v8 benchmark is the canonical number.

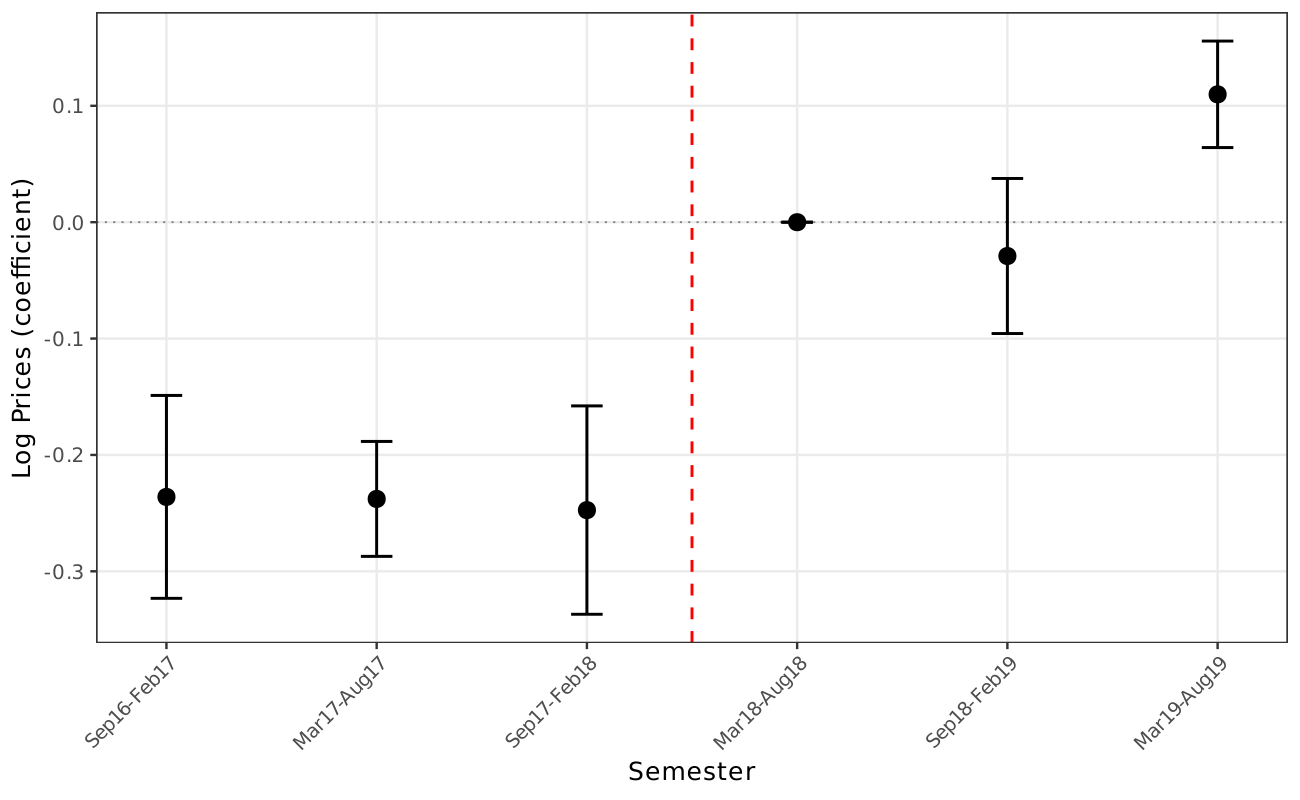

The estimate is stable across 6/12/18-month windows around the March 2018 PGE-SP legal reversal, robust to PBU fixed effects, and concentrated at the lower end of the conditional price distribution: quantile DiD finds the effect at \(\tau \leq 0.50\) (β strongly negative) but reversing at \(\tau = 0.90\) (AN-007). Lee (2009) selection bounds are tight, confirming negligible completion-selection bias (AN-005); HonestDiD CIs survive substantial M̄ violations (AN-006); the pre-treatment placebo on prices is null (AN-004).

Event study (figure A.1 / fig_01_logprices_es): semester-by-semester group-65 vs control gap in log prices. The gap moves sharply at the March 2018 cutoff and stabilizes — read for timing and direction. The joint pre-trend test rejects flatness, so the paper does not claim clean pre-period parallel trends; identification of the magnitude is structural.

Caveat. The reduced-form coefficient is a policy comparison under DiDiR identification, not a structural counterfactual. It does not decompose the price gap into the lost-discipline channel and the protected-pool offset (the structural reading lives in Exclusion dominates the price decomposition and rests on the maintained IPV-clock interpretation). The reading is 🟡 because it is a single-source own-project estimate; promotion to 🟢 would require either an independent replication in another procurement jurisdiction or a converging recovery from the Convite first-price sample (cross-modality check; partly run, not yet documented as an AN).

Sources.

- Own analysis: AN-001 (DiDiR price tables), AN-004 (placebo), AN-005 (Lee bounds), AN-006 (HonestDiD), AN-007 (quantile DiD).

- Reports: PGE-SP opinion (March 2018) is the institutional anchor.

- News anchors: none direct.

- Cross-refs: H:price-discipline-loss; H:parallel-trends-hold; docs/results.md main-results page.

- Validation: backing scripts

scripts/02_analysis.R,scripts/05_robustness.R,scripts/07_advanced.Rproduceoutput/tables/tab_prices.tex,tab_placebo.tex,tab_lee_bounds.tex,tab_quantile_did.tex.