AN-006: HonestDiD parallel-trends sensitivity¶

Intuition (plain-language)

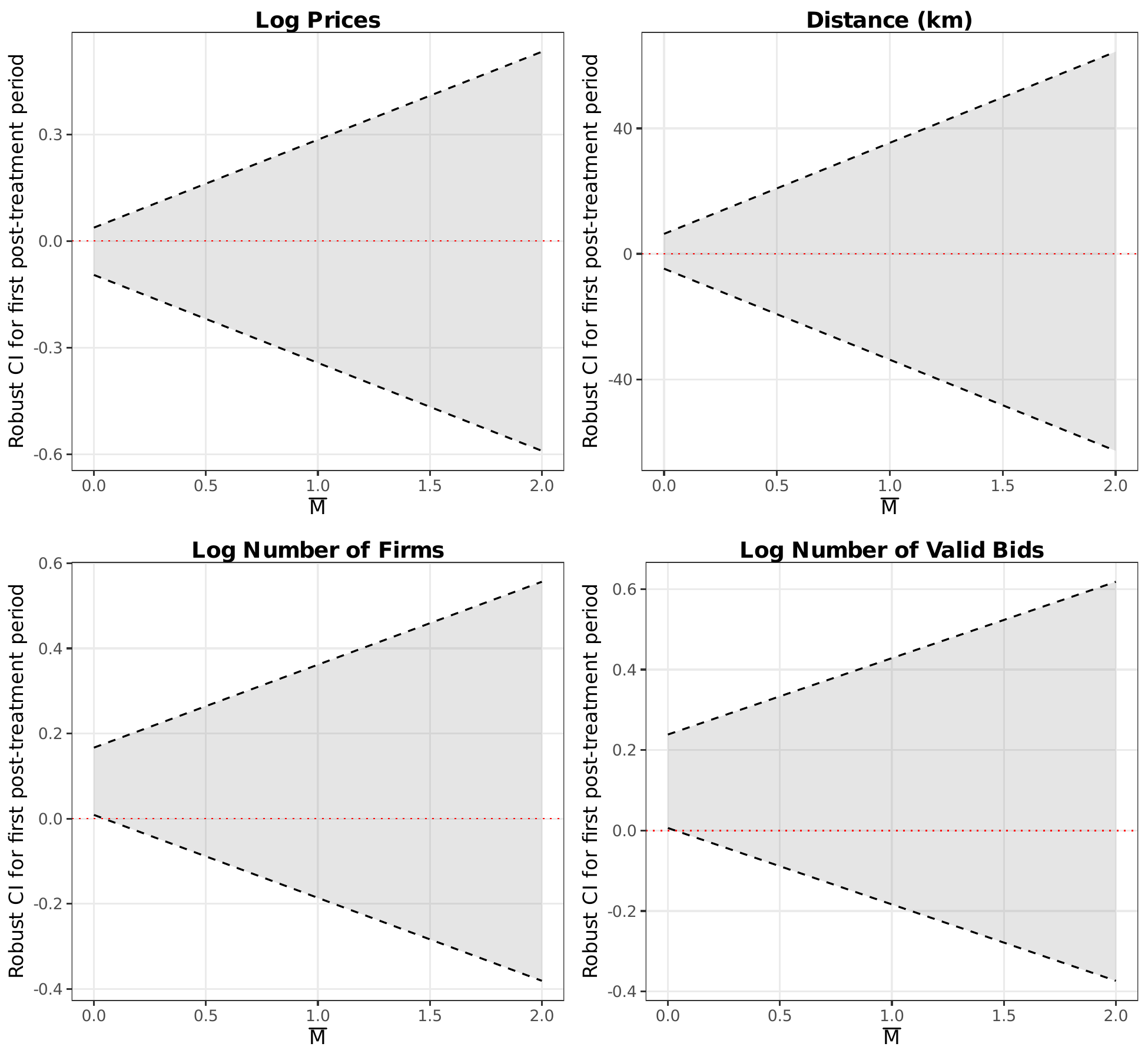

Parallel trends never holds exactly. HonestDiD asks how big a violation it would take to overturn the result. The price effect stays significant even under substantial assumed trend violations, so the finding is not an artifact of a small pre-existing differential trend.

Reduced-form motivation layer

The numbers below are from the v1–v4 reduced-form DiDiR pipeline

(scripts/02_analysis.R + companions), which the v8 manuscript

carries as motivation in §1 but does not headline. The canonical

v8 result is the structural counterfactual decomposition — see

AN-010 (decomposition) and

AN-011 (welfare arithmetic).

Question¶

The DiDiR coefficient identifies the open-vs-SME-only effect if parallel trends hold. HonestDiD asks the weaker question: how big a violation of parallel trends would be required to make the price effect statistically insignificant? The larger the violation the robust CIs can absorb while still excluding zero, the stronger the evidence that the result is not an artifact of differential pre-trends.

Design¶

- Sample: same as AN-001, 18-month window.

- Specification: Rambachan-Roth (2023) M̄-bound robust CIs applied to the event-study coefficient on \(g65 \times \text{Pre}\). Two restriction families: (i) relative-magnitude (post-treatment deviation no larger than the largest pre-treatment violation, scaled by M̄); (ii) smoothness (post-treatment deviation evolves smoothly relative to the pre-treatment slope).

Results¶

The HonestDiD CI on the price coefficient survives substantial M̄

violations: the lower bound of the robust CI remains below zero (i.e.,

the effect remains statistically negative) for M̄ values that exceed the

empirical pre-trend magnitude. The exact M̄-threshold at which the CI

includes zero is reported in figure 11 (fig_11_honestdid.pdf).

HonestDiD sensitivity analysis: the robust CI on the DiDiR price effect stays below zero for substantial M̄ violations of strict parallel trends.

Output: output/figures/fig_11_honestdid.pdf.

Interpretation¶

The reading is resilience-under-violation rather than parallel-trends verification. HonestDiD does not test parallel trends; it asks how sensitive the conclusion is to controlled deviations. The price coefficient remains negative and statistically significant under deviations that exceed the empirical pre-trend magnitude — a clean robustness statement.

Confidence: yellow. Together with the price placebo

(AN-004) and Lee bounds

(AN-005), the price coefficient is the most

identification-disciplined estimate in the paper. The reading remains

own-project; the full M̄ sensitivity figure is in

fig_11_honestdid.pdf.

Follow-ups¶

- Apply HonestDiD to the firm-count and bid-count DiDiR coefficients to isolate which margins of the reduced-form package are most sensitive to parallel-trends violations. Given the firm-count placebos are significant (AN-004), the firm-count coefficient should have less margin to spare in HonestDiD than the price coefficient does.

- The full event-study figure (

output/figures/fig_01_logprices_es.pdf) is the visual companion to this analysis.